Resilient: A single word to capture the U.S. economy over the past five years. It’s remained on solid footing despite an unprecedented upheaval and equally dramatic recovery. But during this period of sometimes-puzzling economic strength, the people haven’t entirely been feeling it: Despite strong numbers on average, consumer sentiment is lackluster.

Economics is a complex, pervasive topic. When you begin to study it, you realize just how much you have to learn. I know that was the case for me, even before graduate school. So, for the general public, misinformation or misunderstandings could certainly prompt part of the gap between sentiment and reality. The easy answer is to assume ignorance. By implying the data is right and the people are wrong, you make it OK for economists, policymakers and journalists to cast aside these “flawed” perspectives.

Whether sentiment is shaping household and broader economic strength or being used by economists to predict spending and saving, how people perceive their economy matters.

This report examines the disconnect between economic data and sentiment, and potential reasons for it. It then discusses why we shouldn’t be too quick to discount how people feel about their economic prospects.

On this page

- Post-Covid: The economy came back strong, sentiment stayed weak

- “Average” experience may not reflect personal experience

- The economy is a high emotion and “hot button” issue

- Information quality varies from source to source

- Increased partisanship increases sentiment gap

- Nostalgia promises the past was better (even when it wasn’t)

- Sentiment as predictor of economic health

- Happiness economics: Well-being may promote economic health

- Exploring the disconnect drives better coverage and communication

Post-Covid: The economy came back strong, sentiment stayed weak

The past five years have been characterized by remarkable times that, in some instances, led to predictable outcomes in the economy. In other instances, there were outcomes we didn’t — and sometimes simply couldn’t — see coming at all.

The global pandemic resulted in the shuttering of businesses, a downturn in spending and thus the most dramatic U.S. recession of the modern era. Just as dramatic was the recovery. In less than two years, the unemployment rate went from nearly 15% to consistently below 4% . In the second quarter of 2020, the economy contracted 33% before essentially making up that ground by year’s end . Coming on the heels of the long, slow recovery of the Great Recession, this one was starkly different.

American consumers, on average, emerged from lockdowns waving cash around. People’s inability to go anywhere and their lower spending created excess savings, bolstered by economic impact payments. This all fueled a tremendous rebound effect after lockdowns, and beyond that in the quarters that followed . Spending would remain strong far longer than initially thought.

Consumer demand remained robust, and supply-chain issues sent inflation soaring. The Federal Open Market Committee began lifting the target federal funds rate in spring 2022 to slow price growth. From there, the Fed raised rates 11 times in 17 months .

“ Despite all of this, regular people haven’t been celebrating the economy. And certainly some discomfort is justified. ”

Many economists and wonks went into this period of monetary policy-tightening expecting a recession, as inflation reached its highest heights since the 1980s. To slow the economy enough to tamp down such historically high price growth required the booming economy as sacrifice. But the strong consumer and labor market have thus far prevented a downturn.

From January 2022 through May 2024, the unemployment rate remained at or below 4%, low by historical standards . Workers found it easy to secure jobs, and many left their current positions for greener pastures: The quits rate hit an all-time high of 3% in late 2021 and early 2022 . Wages rose, and rose particularly fast among the lowest-earning households, while asset values climbed unabated.

Despite all of this, regular people haven’t been celebrating the economy. And certainly some discomfort is justified. Prices on goods and services remain high. While inflation has subsided considerably, adjusting to higher prices takes time. Also, the housing market is possibly playing an outsized role, plagued by low inventory and high prices, and magnified by high mortgage rates. And high rates overall make it more difficult to finance large purchases, expand your small business or pay down a credit card balance.

Sentiment has suffered since the pandemic recession

While the economic recovery post COVID-recession may have been swift, consumer sentiment didn’t recover in the same way.

The University of Michigan’s Index of Consumer Sentiment, available since 1952, is one of a few trusted and longstanding sources of overall consumer economic confidence, consisting of five questions to gauge how people are feeling about the current and future economy and their household’s place within it. That sentiment score hit an all-time low of 50 in June 2022 — lower even than in 1980, when inflation peaked near 15%; then, the consumer sentiment index averaged 65. Since that 2022 low, it’s recovered modestly to 67.8 as of August 2024, a rise the director of the program called “stubbornly subdued.”

Another source of consumer sentiment data, The Conference Board’s Consumer Confidence Index, created in 1967, also remains below prepandemic levels.

Three in 5 Americans (60%) said they believed the U.S. economy was currently in a recession in mid-July, according to NerdWallet’s most recent survey on the health of the economy, conducted online by The Harris Poll. Official determination of a recession is made in hindsight by the National Bureau of Economic Research, so it’s somewhat normal for people, even experts, to try and make that call in real time. However, current economic data doesn’t indicate a recession.

As of the writing of this piece, unemployment has risen and the labor market is cooling but strong. Growth in consumer spending is showing signs of slowing, but the economy continues to expand.

Why feelings and data diverge

“Average” experience may not reflect personal experience

Economic data is most often estimates coming to us in large aggregates — averages, medians — and is often reported by the movements of these estimates from month to month, or year to year. Though each calculation gets the numbers closer to something that resembles the nation as a whole, or at least something that is far simpler to grasp, the United States is a large country, with very disparate economic conditions. So each calculation can also serve to get us further away from the lived, individual experiences.

For example, wages grew 19% from July 2020 through July 2024, according to the Bureau of Labor Statistics, slightly slower than inflation during that same period (21%). But not everyone experienced 20% pay increases during the four-year period. For example, the information sector saw wages rise 13% during that period, whereas wages in leisure and hospitality rose 31%. And again, within these averages there are workers who saw lower and much higher increases. How your wages grew (or didn’t) is likely to significantly impact your outlook on the economy, particularly during a high inflation period.

Indeed, there is evidence people judge the health of the overall economy based on their own, potentially unique, experiences. When asked in our July survey where they get information about the health of the U.S. economy, 34% of Americans cited “personal experience” among their answers — it was one of the most cited sources of economic information.

Increasing inequality, wealth effects could widen this gap

Even households fortunate enough to experience notable income increases over the past several years have found it doesn’t necessarily equate to rising wealth or economic stability.

In 2019, the Federal Reserve reported that 63% of American adults said they could cover an unexpected $400 expense with cash or cash equivalents, a sign of financial resiliency. That share peaked at 68% in 2021, as households across the income spectrum benefited in part from economic impact payments. In 2023, however, it returned to 63% .

The lowest earners experienced the greatest real wage growth through the end of 2022, but that is no longer the case, according to researchers with the Minneapolis Fed. Wage growth among the lowest earners now, in 2024, is lower than it was in 2019 . These populations may have played a role in the overall consumer resiliency early in the inflationary period, but ongoing spending strength could now be coming solely from higher earners. People with plenty to spend could be carrying the aggregate, so to speak.

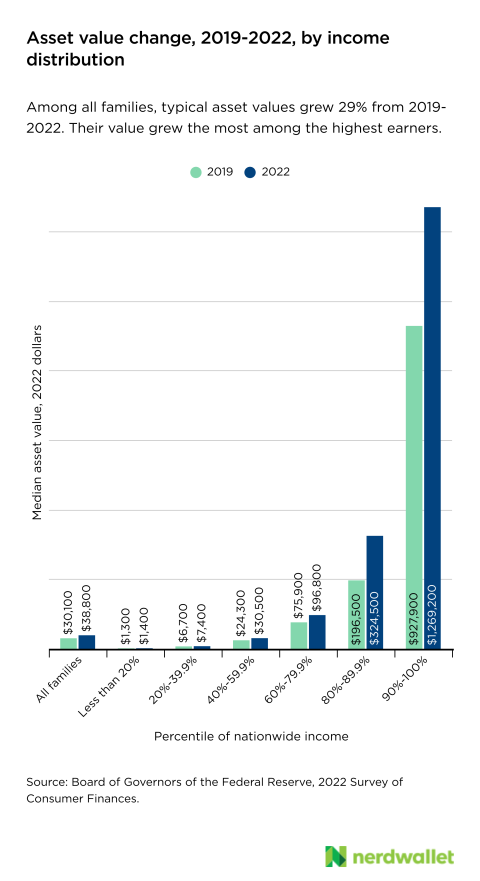

In addition to income, financial well-being is driven by wealth, and wealth is built with assets. From 2019 to 2022, the real median value of assets for the top-earning 10% grew 37%, from about $928,000 to $1.27 million, according to data from the Federal Reserve’s Survey of Consumer Finances. Meanwhile, the median value of assets among the lowest-earning 20% grew from $1,300 to $1,400, just 8%.

It stands to reason that households earning the least and with the least financial insulation could be the most displeased about the economy, and this could cloud their perspective. Indeed, we found lower earners are more likely to think inflation is higher now than it was one year ago, perhaps in part because they’re more sensitive to prices.

But individual experiences can’t wholly explain the difference in economic sentiment and economic data. If they could, you’d expect people to feel about equally as bad about their own finances as they do about the broader economy. Yet when we asked in an April 2024 survey conducted online by The Harris Poll, half (49%) of Americans said they felt worse about the state of the U.S. economy in general compared to 12 months ago, though only 29% said they felt worse about the state of their own personal finances over the same one-year period.

About 4 in 5 Americans (81%) say the economy is a “hot button” issue, one that is controversial or high-emotion, according to our July survey. And when there are high emotions tied up in a topic, it’s difficult to not let those emotions influence your perspectives.

In the April survey, we asked Americans whether they were feeling better or worse about economic and financial conditions compared with 12 months prior. Of the things we asked about — including personal finances, access to credit, ability to manage debt, and the ability to cover the costs of necessities — the state of the U.S. economy in general garnered the strongest feelings. It was this topic that garnered the fewest neutral (“neither worse nor better”) responses (25%). In fact, roughly half (49%) said they felt worse about the economy than they did 12 months ago.

The strength of feelings about the economy in general could make it easier to divorce sentiment from reality. Over the past several years, with the inundation of misinformation online, researchers have had ample opportunity to explore the role of emotion in identifying bad information. The bottom line: People use emotions as information to form beliefs in much the same way they use facts . So, when you feel a certain way about a topic, those feelings can determine what you believe to be true. And when information is portrayed in a way that’s more likely to play into your emotions, these effects can be compounded .

Information quality varies from source to source

The quality of the information we’re exposed to impacts our beliefs, whether that information is conveyed in an emotional manner or not. Regardless of our household financial situation, if we’re being told the economy is bad by a source we trust, we may feel like the economy is bad regardless of what other evidence says. In this way, both good (accurate) and bad (inaccurate or misleading) information can spread.

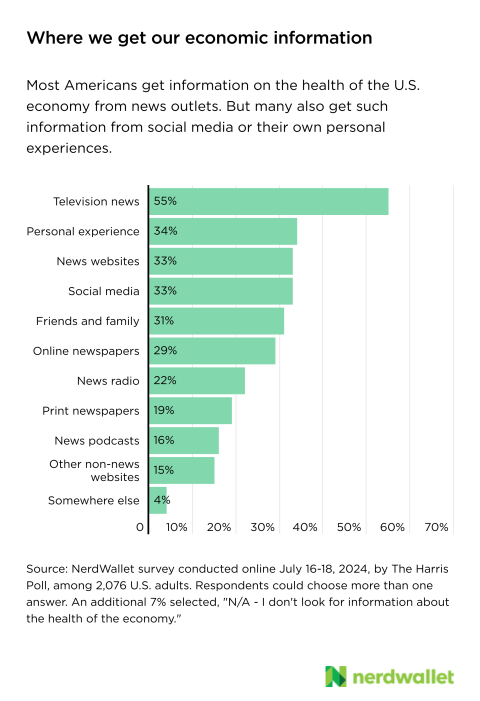

More than half of Americans (55%) get information about the health of the U.S. economy through the television news — a source most popular among baby boomers (69% ages 60-78 vs. 43% Gen Z ages 18-27, 41% Millennials ages 28-43, and 58% Gen X ages 44-59). Roughly equal shares of Americans get such information from personal experience (34%), news websites (33%) and social media (33%). While any one of these sources can provide good information, none offers a complete picture.

An additional 31% of Americans get their information on economic health from friends and family. The people around us shape our perceptions. And certainly, anecdotes are powerful. So even when we have a job we enjoy, for example, where we feel appropriately compensated and secure, and even when unemployment is low, if we hear about a friend or relative who lost their job and has had trouble finding a replacement, we may first think of them when we think of labor market health.

And this is a slippery slope — bad information can lead to more bad information. Confirmation bias tells us that when we believe something to be true, we seek out more information to confirm those existing beliefs.

Increased partisanship increases sentiment gap

Partisanship could be increasing the gap between economic reality and sentiment, and helping to fuel the bad information loop. This problem may be felt at a unique magnitude in the U.S. — political polarization is growing more rapidly here than in other similar democratic nations, according to researchers with Brown University .

A look at consumer sentiment index scores broken out by respondent political parties provides insight. Consumer sentiment as a whole fell, beginning with the onset of the COVID pandemic, but there was a clear shift in perspective during the 2021 presidential administration change, and before that, to a lesser extent, in 2017. Right or wrong, when the political party you align with is in power, there’s a better chance you’ll feel better about the economy overall.

We see this potentially reflected in some of the data from our most recent survey. Seven in 10 (70%) Republicans believed that the U.S. economy was in a recession when we asked in July, compared with 53% of Democrats and 58% of Independents. At this same time, 72% of Republicans said inflation was higher in July than last year at that time, a sentiment shared by 58% of Democrats and 60% of Independents. This when inflation as measured by the Consumer Price Index was 2.9% at the time of the survey and slightly higher, 3.3%, in July 2023.

Our interpretations of current economic conditions may be skewed by our personal situation, our information sources and our political parties. Our perspectives of the past aren’t perfect either.

Nostalgia promises the past was better (even when it wasn’t)

Whatever your impressions of the economy are, it’s much easier to take stock in the present than it is to remember what they were a few years ago. Whether it’s high prices or high interest rates, if you have certain economic factors presently causing you pain, they’ll likely weigh more heavily on your overall views of current economic health.

Remembering the economy of the past as pleasant can stand to magnify that present day discomfort.

If you asked me to recall the summer of 2010, I’m far more apt to remember the beach trip I took with my 10-year old daughter, and not the record foreclosure rates in the wake of the Great Recession.

When asked how they remember the strength of the economy at certain key points in recent history, many Americans (38%) remember the summer of 2010 as being strong, whereas just 24% say the economy was weak. In the more recent past, 31% of Americans remember the summer 2020 economy as strong and 41% as weak. Recall during the summer of 2020, we were emerging from pandemic lockdowns and unemployment sat around 10%.

One explanation for the misremembering is what’s called fading affect bias: where the emotions tied to negative events fade faster than those related to positive ones. Further, and relatedly, talking about the good times is just a more pleasant conversation than talking about the bad times, so it’s likely we’ve revisited the bad less often.

The housing market provides a good illustration of nostalgia versus data, and the nuances involved. Yes, the number of available homes for sale is paltry, prices are incredibly high and high mortgage rates are only exacerbating affordability issues. But in a November 2023 survey for our 2024 Home Buyer Report, 66% of Americans said that current mortgage rates were unprecedented, which we defined as “having never been what they are now.” In fact, at the time of the survey, the average rate on a 30-year fixed mortgage was 7.2%. Previously, it broke 8% in 2000, and before that it peaked over 10% in 1990 and 18% in 1981. Rates are certainly high, but they’ve also been here (and higher) before.

It’s true that many people buying homes today were not buying homes when rates were previously this high. But it’s not only the youngest among us misremembering (or romanticizing) economic conditions of the past. And yes, homes were more affordable in the 1960s, but households were generally less well off. Homes were far less likely to have multiple bathrooms or laundry facilities, dining out was reserved for special occasions like birthdays, and air travel was accessible to only the wealthy .

The disconnect between economic data and sentiment most likely exists for numerous reasons, and in each individual to varying degrees. And while it would be easiest to simply disregard negative sentiment in the face of strong economic data, the easy route isn’t likely the most responsible.

Why (even inaccurate) feelings about the economy matter

Sentiment as predictor of economic health

Consumer sentiment holds some predictive value for economic health, namely in spending behaviors. If people are feeling bad about the economy, and particularly if they’re feeling bad about the near-future economy, they’re likely to spend less and perhaps save in a precautionary way. If they’re feeling good, they’ll spend freely. This can also be a self-fulfilling prophecy. Consumer spending, as discussed, has the potential to drive economic strength. So, if people feel good about the economy, they spend more, which then drives a healthier economy, which makes them feel good, and spend more, and so on.

On its face, this makes sense, and would not only underscore the importance of consumer sentiment, but help explain why it could be divorced from the data — if, in fact, it leads or precedes the data. In this case, perhaps the people know something not yet being registered by the official data sources.

Happiness economics: Well-being may promote economic health

Setting the predictive value of sentiment aside, perhaps we should just care about how our communities feel. If people feel like they're struggling or feel like the economy is against them, that can impact their general life satisfaction. And don’t we want our fellow humans to enjoy the time they have?

Beyond simply wanting people to be content or even happy for the sake of it, happiness economics explores the impact of the economy on personal well-being, and the impact of well-being on the economy.

The very things we often associate with life satisfaction are those that are made possible with a healthy, productive economy. Clean air and water, proper health care and nutritious food, leisure time to spend with the people we care about and more public support for the arts — these are ideas that make life more enjoyable and are more often features of wealthy economies.

And this channel also flows in the other direction. Think about when you’re most productive and creative — it’s unlikely when you’re feeling depressed or overwhelmed. It’s through these channels — productivity and creativity — that life satisfaction can promote a healthier economy. The feel good, work smarter equation doesn’t only apply at an individual level, but at a business and nationwide level . In this way, positive sentiment could be a meaningful consideration in driving effective policy.

Exploring the disconnect drives better coverage and communication

This could all translate into a fairly big responsibility for people who make their living talking or writing about the economy and the facets of life impacted by it. True, there may be little hope of influencing the deep-rooted psychology of nostalgia, for example, but the duty to convey accurate information in an understandable way is a serious one. One which can impact not only people’s perception of the economy, but their well-being because of it.

Further, a sense of empathy can go a long way. There is a cacophony of economic information when we read the news, scroll social media or have dinner with friends. Purveyors of helpful and accurate information are another voice in the crowd, particularly if they aren’t speaking to a specific audience with specific intent. Understanding and conveying good economic information is a start, but being a trustworthy source requires acknowledging that your audience is operating from a variety of different perspectives. Good data can tell you what’s happening in the aggregate, but that can be markedly different from what an individual is experiencing and particularly divergent from how they’re feeling about it.

“ Good data can tell you what’s happening in the aggregate, but that can be markedly different from what an individual is experiencing and particularly divergent from how they’re feeling about it. ”

Methodology

The July survey was conducted online within the United States by The Harris Poll on behalf of NerdWallet from July 16-18, 2024 among 2,076 U.S. adults ages 18 and older. The April survey was conducted online within the United States by The Harris Poll on behalf of NerdWallet from April 2-4, 2024 among 2,061 U.S. adults ages 18 and older. The sampling precision of Harris online polls is measured by using a Bayesian credible interval. For these studies, the sample data is accurate to within +/- 2.5 percentage points using a 95% confidence level. For complete survey methodologies, including weighting variables and subgroup sample sizes, please contact [email protected].

Disclaimer

NerdWallet disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the article’s information is accurate, reliable or free of errors. Use or reliance on this information is at your own risk, and its completeness and accuracy are not guaranteed. The contents in this article should not be relied upon or associated with the future performance of NerdWallet or any of its affiliates or subsidiaries. Statements that are not historical facts are forward-looking statements that involve risks and uncertainties as indicated by words such as “believes,” “expects,” “estimates,” “may,” “will,” “should” or “anticipates” or similar expressions. These forward-looking statements may materially differ from NerdWallet’s presentation of information to analysts and its actual operational and financial results.

Article sources

NerdWallet writers are subject matter authorities who use primary,

trustworthy sources to inform their work, including peer-reviewed

studies, government websites, academic research and interviews with

industry experts. All content is fact-checked for accuracy, timeliness

and relevance. You can learn more about NerdWallet's high

standards for journalism by reading our

editorial guidelines.

- 1. U.S. Bureau of Labor Statistics. Unemployment Rate, retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 2. U.S. Bureau of Economic Analysis. Real Gross Domestic Product, retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 3. U.S. Bureau of Economic Analysis. Personal Consumptions Expenditures, retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 4. Board of Governors of the Federal Reserve System (US). Federal Funds Target Range - Upper Limit , retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 1. U.S. Bureau of Labor Statistics. Unemployment Rate, retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 1. U.S. Bureau of Labor Statistics. Unemployment Rate, retrieved from FRED, Federal Reserve Bank of St. Louis. Accessed Aug 19, 2024.

- 7. Board of Governors of the Federal Reserve System (US). Report on the Economic Well-Being of U.S. Households in 2023 - May 2024. Accessed Aug 19, 2024.

- 8. Wozniak, A., Horwich, J., Cowles, K.. Is Real Wage Growth Sustainable? Evidence from Real Wage Growth Across Groups - July 2024. Accessed Aug 19, 2024.

- 9. Ecker, U., Lewandowsky, S., et. al. The Psychological Drivers of Misinformation Belief and Resistance to Correction - Nature Reviews Psychology. Accessed Aug 19, 2024.

- 10. Carrasco-Farre, C. The Fingerprints of Misinformation: How Deceptive Content Differs from Reliable Sources in Terms of Cognitive Effort and Appeal to Emotions - Humanities and Social Sciences Communications. Accessed Aug 19, 2024.

- 11. Boxell, L., Gentzkow, M., Shapiro, J. Cross-Country Trends in Affective Polarization — National Bureau of Economic Research, 2020. Accessed Aug 19, 2024.

- 12. Sarkar, M. How American Homes Vary by the Year They Were Built - U.S. Census. Accessed Aug 19, 2024.

- 13. DiMaria, C., Peroni, C., Sarracino, F. Happiness Matters: Productivity Gains from Subjective Well-Being - Journal of Happiness Studies, 2019. Accessed Aug 19, 2024.

- 14. Oswald, A., Pronto, E., Sgroi, D. Happiness and Productivity, Journal of Labor Economics. Accessed Aug 19, 2024.

- 15. Lee, Y., Goh, K. The Happiness-Economic Well-Being Nexus: New Insights From Global Panel Data. Accessed Aug 19, 2024.