We believe everyone should be able to make financial decisions with

confidence. While we don't cover every company or financial product on

the market, we work hard to share a wide range of offers and objective

editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that

appear on our site. This compensation helps us provide tools and services -

like free credit score access and monitoring. With the exception of

mortgage, home equity and other home-lending products or services, partner

compensation is one of several factors that may affect which products we

highlight and where they appear on our site. Other factors include your

credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot

pay us to guarantee favorable reviews. Here is a list of our partners.

Coverdash Insurance Brokerage Review 2025

Coverdash is an online broker that can get insurance quotes for your business.

Many, or all, of the products featured on this page are from our advertising

partners who compensate us when you take certain actions on our website or

click to take an action on their website. However, this does not influence our

evaluations. Our opinions are our own. Here is a list of our partners and

here's how we make money.

Published · 3 min read

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and

relevance. It undergoes a thorough review process involving writers and

editors to ensure the information is as clear and complete as possible.

Rosalie Murphy has covered small-business banking, credit cards, insurance and lending at NerdWallet since 2021. She writes and edits the Starting Small newsletter, and her reporting has appeared in publications like the Associated Press, MarketWatch and Nasdaq. Rosalie is an MBA candidate at Kent State University and has a bachelor's degree in journalism from the University of Southern California.

Ryan Lane is an editor on NerdWallet’s small-business team. He joined NerdWallet in 2019 as a student loans writer, serving as an authority on that topic after spending more than a decade at student loan guarantor American Student Assistance. In that role, Ryan co-authored the Student Loan Ranger blog in partnership with U.S. News & World Report, as well as wrote and edited content about education financing and financial literacy for multiple online properties, e-courses and more. Ryan also previously oversaw the production of life science journals as a managing editor for publisher Cell Press. Ryan is located in Rochester, New York.

Published in

Managing Editor

SOME CARD INFO MAY BE OUTDATED

This page includes information about these cards, currently unavailable on

NerdWallet. The information has been collected by NerdWallet and has not

been provided or reviewed by the card issuer.

Coverdash is an insurance broker that can help you generate quotes and buy business insurance through its partners. Then, you can use Coverdash to pay your premiums, file claims and update your coverage as needed.

If you have relatively simple insurance needs — for example, if you need general liability or workers’ comp insurance to comply with contracts or state laws — Coverdash offers an efficient shopping experience. Quotes come from reputable insurance companies, and the platform provides plenty of detail to help you make an informed decision.

Unfortunately, you can't get a digital quote for commercial auto insurance — though you can talk to an agent about additional coverages you might need. In general, if your company has highly specialized insurance needs, a broker you can talk to in person is probably your best bet.

Coverdash insurance: Pros and cons

Pros

Get multiple quotes for general liability, professional liability, business owners’ policies, D&O and workers’ comp insurance with one application.

Pay premiums and file claims through the Coverdash platform.

Coverdash’s insurance partners include some of NerdWallet’s top-rated business insurance companies, including Chubb, Travelers and Nationwide.

Cons

No digital quotes for commercial auto insurance (though you can talk to an agent for auto quotes).

Coverdash is a brokerage, not an insurance company. Your coverage will be provided by a third party.

How Coverdash works

Coverdash gets insurance quotes from multiple companies based on the information you provide. You’ll need to offer:

Basic information like your name, phone number, email address and business website, if you have one.

Your business type, legal structure, industry, address and year founded.

Annual estimated revenue and payroll.

After that, Coverdash will generate quotes from its partners.

👋 I’m Rosalie Murphy, NerdWallet’s writer covering business insurance. Here’s what you can expect when you get a quote from Coverdash.

I told Coverdash I operated a new, one-person home business as a florist and needed general liability insurance. I predicted $10,000 in annual revenue. (This is hypothetical; sadly, I’m not a florist on the side.)

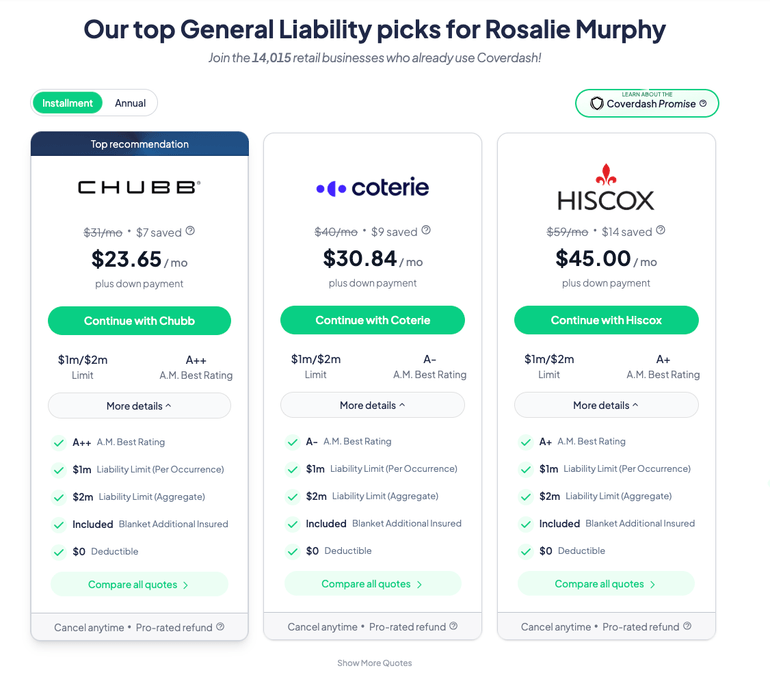

In less than a minute, the service provided multiple quotes for a general liability policy:

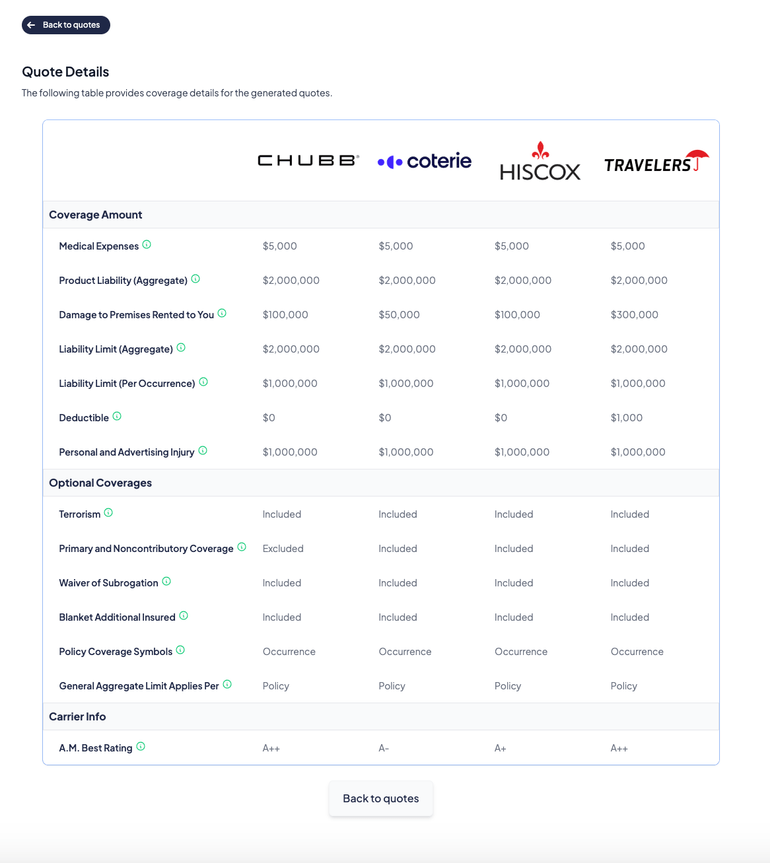

When I dug deeper, Coverdash provided a helpful table that let me compare coverage limits, deductibles and additional coverages. This made it easy to identify differences in policies relative to their prices:

Overall, these policies are quite similar. But for instance, Chubb — the cheapest quote — actually offers more coverage for damage on rented premises than Coterie, which is slightly more expensive.

Chubb doesn’t include primary and noncontributory coverage, though. That means Chubb’s policy won’t pay out before any others that might cover the same claim. For my hypothetical floral business, that probably doesn’t matter. However that coverage is sometimes required for other professions, like contractors.

While I didn’t select an insurer, I did have to provide contact information to see their quotes. Coverdash followed up via email and with two phone calls the next day. (The calls didn’t continue after that, which is always a concern with services like this.)

My quote was also saved when I logged in the next day.

Coverdash insurance: Types of coverage

Through its partners, Coverdash offers the following policies:

General liability insurance protects your business in case of third-party claims of bodily injury and property damage. NerdWallet recommends that all business owners carry a general liability policy. Some leases and contracts require you to have this coverage.

🤓Nerdy Tip

If your business has a physical location, consider a business owner’s policy instead. BOPs include general liability insurance along with commercial property insurance, which pays out if your stuff is destroyed in a covered event like a fire. Most also include business interruption insurance, which helps cover your expenses while you’re making repairs and can’t operate normally.

For businesses with less than $1 million in revenue, Coverdash says the general liability policies it sells usually have premiums in these ranges:

Retail businesses: $700-$1,500 annually.

Professional, scientific and technical services: $700-$1,300 annually.

Wholesale trade: $700-$2,500 annually.

Accommodation and food services: $1,000-$3,000 annually.

Workers’ comp is required in most states, though which companies need it varies by industry and how many employees you have. Coverage kicks in if one of your employees is injured on the job and needs medical care and time off to recover.

Workers’ comp costs can vary widely depending on your industry. For instance, construction businesses tend to have the highest costs since construction workers generally have more risk of injury than retail workers.

For businesses with less than $1 million in revenue, Coverdash says the workers’ comp policies it sells usually have premiums in these ranges:

Retail: $500-$1,600 annually.

Wholesale trade: $500-$1,600 annually.

Accommodation and food service: $900-$2,500 annually.

Construction: $1,000-$10,000 annually (varies by state and what services the company provides)

Many businesses need: Professional liability insurance

Professional liability insurance, also known as errors and omissions insurance, protects your business in case a client accuses you of negligent or inadequate work. If you provide services to customers for a fee, you should have E&O insurance.

For businesses with less than $1 million in revenue, Coverdash says the professional liability policies it sells usually have premiums in these ranges:

Professional, scientific and technical services: $800-$3,500 annually.

Construction (a specific E&O policy for contractors): $1,200-$5,000 annually.

NerdWallet writers are subject matter authorities who use primary,

trustworthy sources to inform their work, including peer-reviewed

studies, government websites, academic research and interviews with

industry experts. All content is fact-checked for accuracy, timeliness

and relevance. You can learn more about NerdWallet's high

standards for journalism by reading our

editorial guidelines.