We believe everyone should be able to make financial decisions with confidence. While we don’t cover every company or financial product on the market, we work hard to share a wide range of offers and objective editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that appear on our site. This compensation helps us provide tools and services - like free credit score access and monitoring. With the exception of mortgage, home equity and other home-lending products or services, partner compensation is one of several factors that may affect which products we highlight and where they appear on our site. Other factors include your credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors’ opinions or ratings, which are based on independent research and analysis. Our partners cannot pay us to guarantee favorable reviews. Here is a list of our partners.

What Is a Schumer Box and How Do You Read It?

A Schumer box is a legally required cheat sheet for credit cards that breaks down two main aspects of any card: interest rates and fees. Here's how to read it and where to find it.

Many or all of the products on this page are from partners who compensate us when you click to or take an action on their website, but this does not influence our evaluations or ratings. Our opinions are our own.

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and relevance. It undergoes a thorough review process involving writers and editors to ensure the information is as clear and complete as possible.

Kenley Young directs daily credit cards coverage for NerdWallet. Previously, he was a homepage editor and digital content producer for Fox Sports, and before that a front page editor for Yahoo. He has decades of experience in digital and print media, including stints as a copy desk chief, a wire editor and a metro editor for the McClatchy newspaper chain.

Paul Soucy has led the Credit Cards content team at NerdWallet since 2015 and the Travel Rewards team since 2023; he is also director of content for Consumer Credit verticals. He was an editor with USA Today, The Des Moines Register and the Meredith/Better Homes and Gardens family of magazines for more than 20 years. He also built a successful freelance writing and editing practice with a focus on business and personal finance. He was editor of the USA Today Weekly International Edition for six years and received the highest award from ACES: The Society for Editing. He has a bachelor's degree in journalism and a Master of Business Administration. He lives in Des Moines, Iowa, with his wife, Sarah; his two sons; and a dog named Sam.

Director of Content

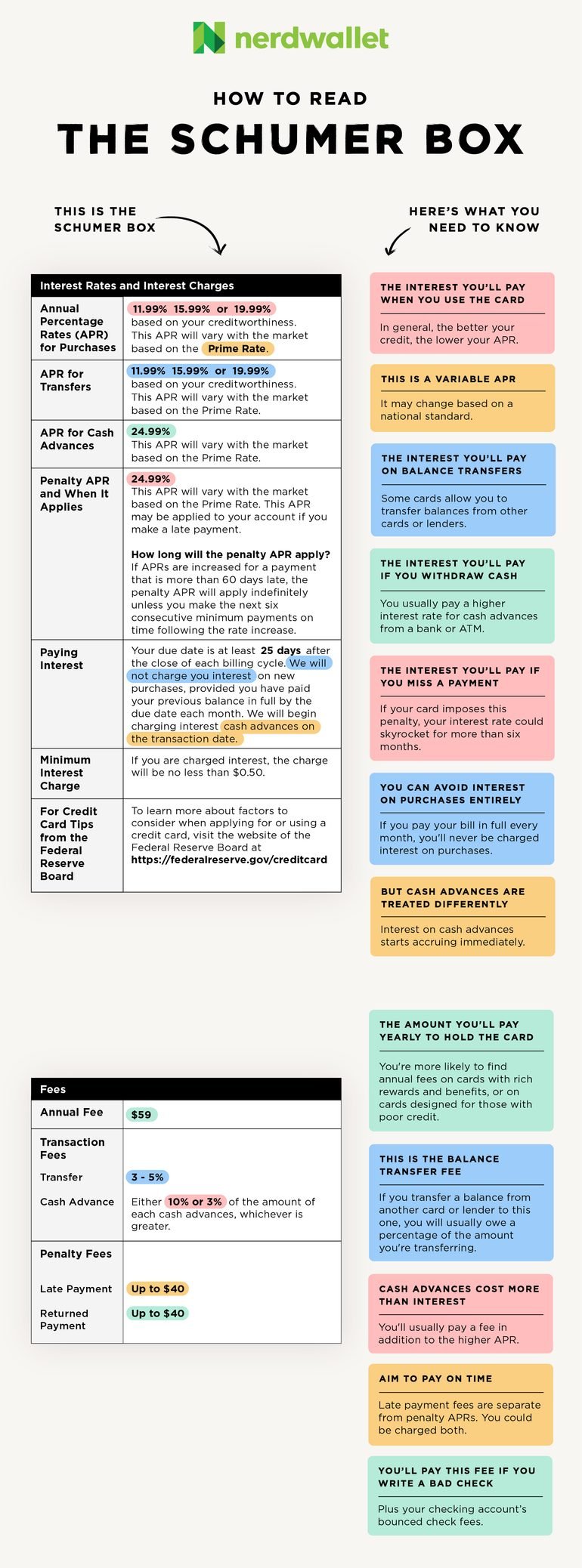

What is a Schumer box? It's a cheat sheet about a credit card — an at-a-glance reference for fees, interest rates and other key points that must be shown to card applicants, by law.

But when it comes to these kinds of credit card terms and conditions, you sometimes need a cheat sheet on reading cheat sheets. Here's our guide to reading and understanding the Schumer box.

Broadly, two main things: interest rates and fees.

1. The credit card's interest rates

These are expressed as APRs ("annual percentage rates"), and usually as variable ranges. This means they can change periodically in step with a benchmark figure called the prime rate — which is the lending rate that banks offer to customers with the best credit. If the prime rate rises, APRs on credit cards tend to do the same.

Those with excellent credit (FICO scores of 720 or higher) will qualify for the lowest APRs.

A card can have multiple APRs depending on the kind of transaction:

For purchases

This is the interest rate you'll be charged when you use the card to pay for things and you carry that balance from month to month. If, however, you pay your credit card bill on time and in full every month, this APR is irrelevant because you will never owe any interest.

Many credit cards come with 0% introductory APR periods on purchases, meaning you'll have a period of time to finance a purchase without paying interest on it.

For transfers

If the credit card allows balance transfers from other lenders, this is the interest rate you'll be charged on those balances when you move them to the card.

Not all cards allow balance transfers, but many that do also offer 0% intro APR periods on such transfers, which can help you pay off existing debt without interest for a period of time — though you may still owe a balance transfer fee. (More on that in the "fees" section below.)

For cash advances

This is the interest rate you'll be charged if you use the credit card to get a cash loan at a bank or ATM. In essence, you're "buying" cash instead of goods or services. While cash advances can be convenient for emergency use, they are also extremely expensive. That's because:

Credit card APRs on cash advances tend to be far higher than APRs on purchases.

Interest on a cash advance begins accruing immediately. You don't get a grace period as you can with purchases.

The card may also impose a fee for the cash advance — either a flat rate or a percentage of the amount advanced. (More on that in the "fees" section below.)

For paying late

Penalty APRs for paying late are a bit less common these days, and even with credit cards that do charge them, they go into effect only under specific circumstances:

If you're only a few days late on your payment, you probably don't have to worry about a penalty APR, but you may still have to pay a late fee. (More on that in the "fees" section below.)

If you're 30 days late or more, you might damage your credit scores, but again there will typically be no penalty APR assessed.

If, however, you pay late by 60 days or more, you could be assessed a penalty APR, which — as with cash advances — is generally much higher than the card's APR on purchases. Moreover, the card issuer can apply that higher interest rate to your entire outstanding balance, not just on new charges going forward. And that penalty APR can remain in effect until you make at least six consecutive on-time payments.

🤓Nerdy Tip

Some credit cards advertise deferred interest deals, aka "special financing." But this is not the same as a true 0% intro APR offer that you might see in a Schumer box. With deferred interest offers, you'll owe no interest if you pay off your entire purchase within the promo period. If, however, any balance remains when that window ends, you'll be charged interest retroactively for the full amount of the transaction, going back to the date of purchase. With 0% intro APR offers, interest is waived, not deferred. When the promo is over, you'll owe interest only on the remaining balance.

Credit cards can charge a variety of fees. Here are some of the most common:

Annual fee

This is the amount you'll pay each year to hold the credit card. Not all cards charge annual fees, but they can be worth paying, depending on the value that the card can deliver back to you.

You're more likely to find annual fees on rewards credit cards that offer rich benefits and incentives, or on cards designed for those with poor credit (FICO scores of 629 or lower).

Balance transfer fee

This is the amount you'll pay for moving an existing balance onto the card. Not all cards allow balance transfers, and not all kinds of debts can be transferred. But the ones that do allow balance transfers tend to charge a fee for doing so, often 3% to 5% of the amount you're transferring.

That could add up to hundreds of dollars tacked onto your balance — but if the card offers a 0% intro APR on balance transfers, it may be worth the cost, depending on how much you're trying to pay off.

If you use your credit card to withdraw cash from a bank or ATM, you'll typically be charged a fee on top of the card's interest rate for cash advances.

The fee will be charged either as a flat rate or as a percentage of the amount that you're withdrawing.

Late payment fees are separate from penalty APRs. Depending on your card and how late you pay, you could end up being charged both. (A new rule proposed by the Consumer Financial Protection Bureau aims to cap credit card late fees at $8.)

Ready for a new credit card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

If you're already a cardholder, the Schumer box will be a hard-to-miss table generally found on the first page of the card agreement that was mailed to you.

If you're researching or applying for a credit card, you may need to click around that card's website to find the Schumer box. It can vary from issuer to issuer, but here's where to start for cards from major issuers:

American Express

Look for a "rates and fees" link.

Bank of America

Look for a link that reads: "View complete list of rates and fees."

Barclays

Look for a "terms and conditions" link. (You may need to scroll to the page footer.)

Capital One

Look for a link that reads: "View important rates and disclosures."

Chase

Look for a "pricing and terms" link.

Citi

Look for a link that reads "pricing details" or "pricing and information."

Discover

Look for a link that reads: "See rates, rewards and other info."

U.S. Bank

References to fees and APRs will often hyperlink to the Schumer box. You can also scroll to the page footer.

Wells Fargo

Look for a link that reads: "Important credit terms."

The Schumer box is named for the lawmaker responsible for it. Chuck Schumer, a congressman and later senator from New York, pushed for legislation requiring that rates, fees and other terms on a credit card be prominently displayed to people when they apply for the card. The legislation passed in 1988, and the standardized disclosure came to be dubbed the Schumer box.

Whether you want to pay less interest or earn more rewards, the right card's out there. Just answer a few questions and we'll narrow the search for you.