Recession Fears and How to Combat Them in 2020

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

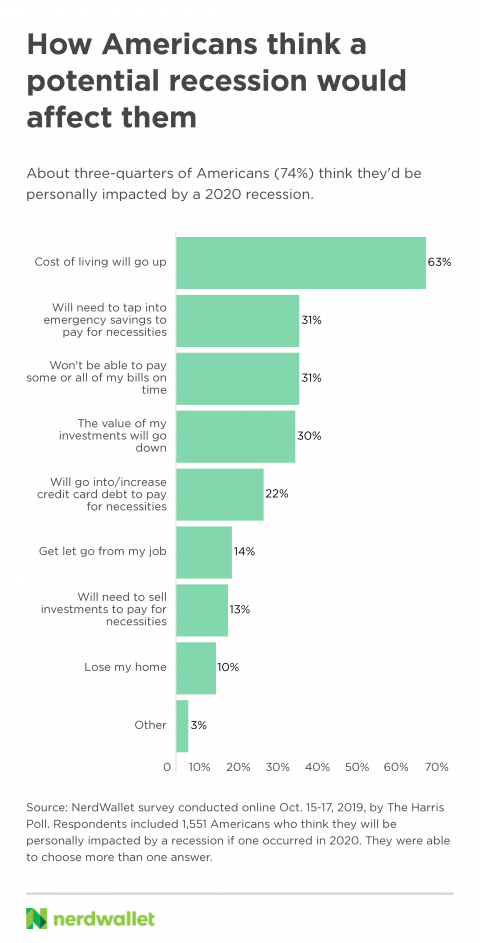

Financial experts have been predicting another recession for years, and about three-quarters of Americans (74%) think they’d be personally impacted if one occurred in 2020, according to a recent NerdWallet survey. Their most common concern is an increased cost of living (63%), but many are afraid of not being able to pay for necessities, plummeting investment value and potential job loss.

Considering the upcoming election, recent interest rate changes and a possible recession, consumers may have concerns about how their individual finances could be affected this year. Here are some common fears that accompany a recession, and what you can do to protect your wallet if they come true.

Fear of needing to tap savings or go into debt for necessities

Close to a third of Americans who think they’d be personally impacted by a 2020 recession (31%) think they would need to tap into emergency savings to pay for necessities. More than 1 in 5 (22%) think they’d need to go into/increase credit card debt for their necessities.

How to combat it: The fear of not being able to pay for necessities is likely tied to the fear of an increased cost of living, so cutting your ongoing monthly spending is a good place to start. Not all expenses can be reduced quickly, but it’s worth looking at your budget for necessities with price flexibility, like car insurance and cell phone plans.

You can also reduce discretionary spending temporarily to build up more of a buffer in your checking account. This extra cash may help you avoid drawing from your emergency fund or swiping your credit card if a recession makes it difficult to pay for necessities.

Fear that the value of investments will go down

Three in 10 Americans who think they’d be personally impacted by a 2020 recession (30%) think the value of their investments would go down. The stock market ebbs and flows, and it’s not unreasonable to feel a little stressed when your investments are dropping in value.

How to combat it: Don’t do anything (in most cases). Stock market losses aren’t realized until you sell. In other words, when the value of your investments go down and you panic and sell them off, you’ve locked in that loss. Whereas if you leave the money in, the value has a chance to rebound. Evaluate your portfolio against your own risk tolerance to make sure stock market volatility won’t keep you up at night, and then avoid obsessing over it.

And if preparing your portfolio for a recession seems too complicated, consider using a robo-advisor to help manage your investments. These computer-aided services cost less than traditional investment management but are designed to automatically rebalance your investments in recessions to help reduce losses.

Avoid overinvesting at the expense of your cash reserves. Invested funds should be earmarked for medium- to long-term goals. Short-term goals — or money you’ll need in less than five years — should be saved for in a high-yield savings account instead. If you feel like you don’t have enough cash accessible in case of recession, you may want to redirect money that you’d otherwise invest into your emergency fund to build up a cushion of three to six months’ worth of expenses.

Earn 3.74% APY by investing in U.S. Treasury Bills*

Maximize your cash by investing in low-risk, government-backed T-Bills. All the work is done for you — just make the deposit and watch your money grow.

Fear of losing a job

About 1 in 7 Americans who think they’d be personally impacted by a 2020 recession (14%) are afraid they’d get let go from their job. After the job losses in late 2008 and 2009 (and beyond), it’s scary to consider losing your primary source of income, particularly if hiring slows and finding a new position becomes more difficult.

How to combat it: Losing your primary income source is an emergency, so make sure you feel comfortable with the amount you have saved. If you find your emergency fund lacking, aim to reduce your expenses in the short term to bulk it up.

As we said before, three to six months’ worth of expenses is a good savings goal, but you can use an emergency fund calculator to determine the right amount for your personal situation. Try not to be discouraged if the ultimate savings goal is more than you can fathom putting away right now. Even $500 or $1,000 saved can be a huge help in bridging the income gap between jobs.

It’s also important to keep your resume updated, so if you haven’t looked at it in a while, now’s a good time. You might also consider diversifying your income sources to soften the financial blow if you lose your job. This means thinking about other ways you can make money, whether that means selling unused items in your home, picking up a part-time job, freelancing, or anything else that helps boost your cash flow.