We believe everyone should be able to make financial decisions with confidence. While we don’t cover every company or financial product on the market, we work hard to share a wide range of offers and objective editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that appear on our site. This compensation helps us provide tools and services - like free credit score access and monitoring. With the exception of mortgage, home equity and other home-lending products or services, partner compensation is one of several factors that may affect which products we highlight and where they appear on our site. Other factors include your credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors’ opinions or ratings, which are based on independent research and analysis. Our partners cannot pay us to guarantee favorable reviews. Here is a list of our partners.

How to Get a Mortgage

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and relevance. It undergoes a thorough review process involving writers and editors to ensure the information is as clear and complete as possible.

Kate Wood is a lending expert and certified financial health counselor (CHFC) who joined NerdWallet in 2019. With an educational background in sociology, Kate feels strongly about issues like inequality in homeownership and higher education, and relishes any opportunity to demystify government programs. Prior to NerdWallet, she wrote about home remodeling, decor and maintenance for This Old House.

Business expert Michael Soon Lee, Ph.D., is an internationally recognized speaker and consultant whose clients include Coca-Cola, Chevron, Boeing, State Farm Insurance and General Motors. He is the author of nine books, including "Black Belt Negotiating” and "Cross-Cultural Selling for Dummies.” Michael has been an award-winning real estate broker since 1980, was licensed to practice taxation before the Internal Revenue Service and is a former certified financial planner who taught taxation for the College for Financial Planning. His articles have appeared in newspapers and magazines such as The Wall Street Journal, the San Francisco Chronicle, the Los Angeles Times and Consumer Reports. He was dean of the School of Management at John F. Kennedy University and served as an adjunct faculty member for Golden Gate University for over 20 years.

At NerdWallet, our content goes through a rigorous editorial review process. We have such confidence in our accurate and useful content that we let outside experts inspect our work.

Amanda is a longtime personal finance editor. She provides content-strategy and leadership support across NerdWallet's verticals. She previously led the international expansion content team (UK, Canada and Australia), and helped lead the mortgages and small-business teams before that. Prior to her time at NerdWallet, Amanda spent 10 years as a content and communications manager in the mortgages and real estate industry. Before that, she was a copy editor for the Contra Costa Times. She has a master’s degree in journalism and is a Dow Jones News Fund alum.

Senior Editor & Content Strategist

Not sure how to get a home loan? Here's a step-by-step guide.

Getting a home loan can be a confusing and stressful process to navigate, but knowing what to expect before you apply can help you stay organized and feel more in control.

1. Give yourself a financial checkup

First, make sure you’re financially prepared for homeownership. Do you have a lot of debt? What have you saved for a down payment? What about closing costs?

A thorough understanding of your income and debts will help you know exactly how much house you can afford. Ideally, your monthly debt payments would account for less than 43% of your income, though some lenders allow for a bit more. This is called your debt-to-income ratio, or DTI. If this amount is 36% or less, you’re more likely to qualify for a low interest rate.

Lenders will also look closely at your credit score. A score of at least 620 will qualify for most loan types, but lenders are more likely to approve you with a higher score — and you’ll also likely receive lower rate offers.

Check your credit score and see if it needs work before you begin applying for a home loan. That can include paying down outstanding debt, disputing errors on your credit reports and not opening any new accounts.

There are many types of home loans available. The one that’s best for you will depend on your financial situation and homeownership priorities.

Conventional loans

These are the most common loans that you’re likely to find among the largest selection of lenders. They have stricter qualification requirements compared with loans insured by the government, so they're a better fit for borrowers with strong credit.

These loans allow for a down payment as low as 3%, but if your down payment is less than 20%, you’ll have to pay for private mortgage insurance, or PMI.

FHA loans are insured by the Federal Housing Administration. These loans can have more lenient credit score minimums (the FHA requires a score of 500) and allow gift money as part of the down payment. FHA loans have a minimum down payment requirement of 3.5%, and you must pay for mortgage insurance for at least 11 years.

VA loans are backed by the Department of Veterans Affairs and are only available to active service members, veterans and some surviving spouses. These loans have no down payment requirements. The VA doesn’t set a minimum credit score; lenders are free to set their own credit requirements. The higher your score, the better your rate offers will be.

USDA loans are backed by the U.S. Department of Agriculture. These zero-down-payment home loans are for borrowers below a set income threshold who live in qualifying areas.

Jumbo loans are for properties valued above the conforming loan limit of $806,500 (or $1,209,750 in certain high-cost areas).

Since these loans aren’t backed by Fannie Mae or Freddie Mac, they’re a little riskier for lenders to offer. This means that they often have stricter requirements, like a credit score in the 700s.

In addition to choosing the type of loan you want, you’ll also have to decide whether you want to apply for a fixed or adjustable interest rate, and select the loan term that makes sense for your budget.

Fixed or adjustable rates

Fixed-rate mortgages are popular because the mortgage interest rate doesn’t change over the life of the loan. The rate to which you initially agree will be the rate you keep until you sell the home or refinance.

Adjustable-rate mortgages (ARMs) have introductory rates that start out fixed, but can then fluctuate. If ARM rates are lower than fixed when you're home shopping, and you don't plan to stay in the home long, an adjustable-rate mortgage could yield savings.

Mortgage terms

A 30-year mortgage is the most common term. Monthly payments are generally smaller than payments with a shorter-term loan, but you’ll pay more interest overall than you would with a shorter-term loan.

Shorter-term house loans, like 10- or 15-year mortgages, are also available. You pay less interest, but monthly payments are generally larger.

» MORE: Use our mortgage calculator to estimate your monthly mortgage payment

3. Research mortgage lenders

Before you start looking at homes, shop around with at least three home loan lenders. There's a wide array of lenders to consider, including traditional banks, online non-bank lenders and credit unions. Consider starting with your own bank or credit union. Some offer lower interest rates for existing customers.

If you're looking for a particular type of mortgage, you may want to zero in on specialty lenders. For example, if you know you want a VA loan, a lender that focuses on working with military borrowers may best fit your needs.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%AmeriSave offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

720720

Min. down payment

N/ANBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

There are a couple of big advantages to getting a mortgage preapproval. One, it shows sellers that you can make a solid offer up to a specific price. Two, it helps you figure out what your mortgage will really cost, since you'll get details on the rate, APR, fees and other closing costs.

It's smart to get preapproved by at least three lenders, as comparing rates could potentially save thousands of dollars over the life of the loan.

5. Submit your application

Even if you’ve been preapproved, you’ll have to submit your most recent financial information after your offer is accepted on a house and you formally apply for a home loan. This can include:

W-2 forms and tax returns from the past two years.

Pay stubs from the past 30 days.

Proof of other sources of income.

Recent bank statements.

Details on long-term debts such as car or student loans.

ID and Social Security number.

Documentation of sources for recent deposits in your bank accounts.

Documentation of any giftsor other funds used for your down payment.

There may be other kinds of documentation required, depending on the type of mortgage you’re getting.

🤓Nerdy Tip

If you’re self-employed, you may have to provide extra proof of your financial stability, including having a higher credit score or large cash reserves, and possibly providing business tax returns.

Within three days of receiving your application, your lender will give you an initial loan estimate, which includes:

How much the loan will cost.

Associated fees and closing costs, including information on which costs you can shop for.

Interest rate and APR, or the annual cost a borrower pays for a loan, including certain fees, such as discount points.

6. Begin the underwriting process

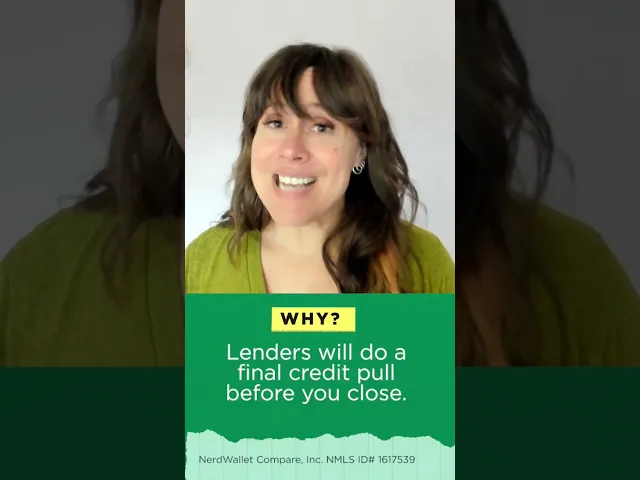

The lender will take a look at your updated credit report and order a home appraisal, which tells the lender the market value of the home you’re buying.

Meanwhile, you’ll schedule a home inspection, which will look for any defects in the home. Depending on how it goes, you may negotiate with the seller for repairs or a lower price before closing.

During the underwriting process, you'll want to avoid making changes to your finances, such as switching jobs or taking out another line of credit. Same goes for large purchases that increase your debt, such as buying a car. Increasing your debt can lower your credit score, which could make the loan costlier — or even jeopardize your qualification.

Finally, your loan is approved! But you’ve got a few more steps to take before the process is complete.

Purchase homeowners insurance. Your lender will require you to do this. Shop around for the best policies.

Buy the lender’s title insurance policy. And although it’s not required, it’s wise to also purchase your own title insurance. Both policies offer protection in case there are problems with the home’s title.

Do a final walk-through of the home. Make sure nothing has changed (and any agreed-upon repairs have been made) since the home inspection.

Review your updated loan estimate and closing disclosure. You'll get this three days before the scheduled closing date. Compare these new documents to what you got when you were initially approved, so you can see if and how any costs have changed unexpectedly.

Get funds for your cash to close. Depending on what your lender requires, you may need a cashier's check from your bank or a wire transfer to pay the final closing costs. Typically, you’ll pay between 2% and 6% of the home’s purchase price in closing costs. You can estimate your expenses using a closing costs calculator.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

N/ANo score credit options are available.

Min. down payment

0%Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%AmeriSave offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

720720

Min. down payment

N/ANBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

If you start having serious second thoughts at this point, you can still walk away. However, you might lose your deposit — also calledearnest money — if you decide not to close.

Don’t be afraid to ask questions of your lender. Getting a mortgage comes with a lot of paperwork. Take the time to understand it all. Know what you’re signing and what you’re paying.

And that’s it — you made it to the top, and the loan is yours. It’s finally time to move into your new home!

How can I increase my chances of getting a mortgage?

You can boost your chances of mortgage approval by paying down structured debts, like car loans, and limiting your credit card usage.

You can also save up a larger down payment. Putting down more cash upfront makes you less of a risk in lenders' eyes. Working to build up your credit score can help, too, both with qualifying for a home loan and getting a better rate.

What kind of credit score do you need to qualify for a home loan?

A credit score of 620 is generally the credit score you need to buy a house. Some government loans allow for lower scores, though in order to qualify with a score under 620 you'd likely need otherwise solid financials or a co-borrower with a stronger score.

How can I increase my chances of getting a mortgage?

You can boost your chances of mortgage approval by paying down structured debts, like car loans, and limiting your credit card usage.

You can also save up a larger down payment. Putting down more cash upfront makes you less of a risk in lenders' eyes. Working to build up your credit score can help, too, both with qualifying for a home loan and getting a better rate.

Which loan is best for first-time home buyers?

First-time home buyers may benefit from loans with low down payment and credit score requirements. Some

. Some government loans allow for lower scores, though in order to qualify with a score under 620 you'd likely need otherwise solid financials or a co-borrower with a stronger score.