RBC Mortgage Rates

Current discounted RBC mortgage rates

Term | Rate | APR |

|---|---|---|

1-year (fixed, uninsured) | 5.24% | 5.37% |

2-year (fixed, uninsured) | 4.54% | 4.60% |

3-year (fixed, uninsured) | 4.39% | 4.43% |

4-year (fixed, uninsured) | 4.49% | 4.52% |

5-year (fixed, insured) | 4.29% | 4.32% |

5-year (fixed, uninsured) | 4.59% | 4.62% |

5-year (variable, insured) | 3.65% | 3.68% |

5-year (variable, uninsured) | 3.95% | 3.98% |

7-year (fixed, uninsured) | 5.00% | 5.02% |

This table is updated daily on weekdays using data available on the Royal Bank of Canada’s website.

Current posted RBC mortgage rates

Term | Rate | APR |

|---|---|---|

1-year (fixed, uninsured) | 5.84% | 5.97% |

2-year (fixed, uninsured) | 5.14% | 5.20% |

3-year (fixed, uninsured) | 6.05% | 6.09% |

4-year (fixed, uninsured) | 5.99% | 6.02% |

5-year (fixed, uninsured) | 6.09% | 6.12% |

5-year (variable, uninsured) | 4.45% | 4.48% |

7-year (fixed, uninsured) | 6.40% | 6.42% |

This table is updated daily on weekdays using data available on the Royal Bank of Canada’s website.

RBC mortgage rates vs. other Canadian banks

3-Year Fixed | 4.42% | 4.41% | 4.44% | 4.43% | 6.05% | 4.624% |

3-Year Variable | 7.78% (open) | 4.17% | -- | -- | 5.95% | -- |

5-Year Fixed | 4.51% (insured) 4.66% (uninsured) | 4.21% (insured) 4.56% (uninsured) | 4.43% (insured) 4.58% (uninsured) | 4.32% (insured) 4.62% (uninsured) | 6.09% | 4.761% (insured) 4.761% (uninsured) |

5-Year Variable | 4.17% | 4.27% | 4.49% | 3.68% (insured) 3.98% (uninsured) | 4.90% | 4.361% |

Rates in bold are discounted annual percentage rates (APR), which include additional fees.

RBC prime rate

As of October 30, 2025, RBC’s prime rate is 4.45%.

RBC’s prime rate is the basis for its variable-rate lending products, like mortgages, credit cards and lines of credit. When the Bank of Canada adjusts its overnight rate, RBC’s prime rate increases or decrease by the same amount, affecting the cost of borrowing for these products.

RBC mortgages: A detailed breakdown

RBC mortgage products

Fixed-rate mortgages.

Variable-rate mortgages.

RBC Homeline Plan, which combines a mortgage and a line of credit.

Home renovation loans.

Mortgages for second homes and investment properties.

Posted vs. special RBC mortgage rates

Posted mortgage rates

Posted rates are the rates RBC makes available publicly. These tend to be the bank’s highest rates because they haven’t been discounted. Think of RBC’s posted rates as you would a car dealership’s sticker prices: They’re a fine starting point for a negotiation, but you’d never want to pay them.

Special mortgage rates

RBC’s special rates are the bank’s posted rates that have been discounted. These might be limited-time offers or the rates a bank offers its mortgage broker partners.

Even if you’re offered a special mortgage rate at RBC, don’t be afraid to try and negotiate a lower one.

Fixed vs. variable RBC mortgage rates

Fixed mortgage rates

With a fixed-rate mortgage, your interest rate will remain the same for the duration of your mortgage term, no matter how much RBC might increase its mortgage rates.

Fixed rates offer stability and predictability, but they can cost you plenty in prepayment penalties.

Like most major banks in Canada, RBC offers a much larger selection of fixed mortgage rates than it does variable mortgage rates. RBC’s fixed rates range from one to 10 years.

Variable mortgage rates

If you opt for a variable rate on your RBC mortgage, the rate could rise or fall many times during your term. When it rises, more of your monthly mortgage payment will go toward interest; when it falls, more will go toward the principal.

Getting a variable-rate mortgage from RBC allows you to switch to a fixed rate mid-term without incurring any penalties. You can also break your mortgage contract to prepay your mortgage and only be charged three-months interest.

Open vs. closed RBC mortgages

Open mortgages

RBC offers a small number of open mortgages, which allow you to increase your mortgage payments or even pay your mortgage in full at any time without penalty.

RBC’s open mortgages are available as one-year fixed-rate or five-year variable-rate options.

Closed mortgages

A closed mortgage imposes annual limits on how much you can prepay your mortgage, and may impose other restrictions on the changes you can make to it mid-term.

Most of RBC’s mortgage products are closed.

Convertible mortgages

If you’re unsure how long a mortgage term you should choose, RBC offers a six-month convertible mortgage product that allows you to extend your term at any time.

Convertible mortgages tend to offer lower rates than open mortgages.

Interest rate vs. APR

When investigating RBC mortgage rates or comparing them to the rates of other lenders, it’s best to use the annual percentage rate (APR) provided rather than the interest rate itself.

APR includes any other fees that might be added to the cost of your mortgage, and gives you a more accurate figure with which to calculate your potential mortgage costs.

Mortgage term lengths at RBC

Between one and 10 years for its fixed-rate mortgages.

Three and five years for its variable rate mortgages.

Six months for its convertible mortgages.

Prepayment privileges at RBC

RBC offers a few prepayment options on its closed mortgages. You can prepay up to 10% of your original mortgage principal once a year. You can also take advantage of RBC’s Double Up feature, which allows you to increase your mortgage payment by up to 100% on any payment date.

How to get the best RBC mortgage rate

As Canada’s largest federally regulated A-lender, RBC follows the country’s strict lending guidelines. That means being offered the best mortgage rates at RBC might require:

Raising your credit score. RBC considers credit scores between 660 and 724 to be “good”, so your credit score will have to be in this range or higher before you’re offered an optimal mortgage rate

Making a larger down payment. Going beyond Canada's minimum down payment guidelines can help you get a better rate offer because it lowers the risk for RBC.

Paying down your debt. If your debt service ratios are too high, RBC may feel you have too much debt to comfortably afford a mortgage. That signals higher risk, which generally means a higher rate.

Shopping around. RBC may not offer you the best mortgage rate. Take a look at the rates other lenders and mortgage brokers are offering.

Negotiating: Never be afraid to ask your RBC mortgage advisor if they can improve on the rate they’ve offered you.

How to apply for a mortgage with RBC

You can apply for a mortgage pre-qualification and pre-approval on RBC’s website. Both forms take just a few minutes and don’t require you to dig up any supporting documentation.

If you’d prefer, you can request an RBC agent to walk you through these processes. If you decide to formally apply for a mortgage with RBC, you’ll learn about how to do that directly rom them; there’s no publicly accessible application form online.

Scroll to the bottom of RBC’s mortgage home page, and you’ll find quick links to start the online pre-approval and pre-qualification forms.

From here, you can also contact an RBC mortgage specialist in your area if you’d prefer assistance with these tasks, or if you’d like to get more information.

Pre-qualificaiton is a quick way to estimate how large a loan you may be approved for. It’s less comprehensive than getting pre-approved. You’ll want to get pre-approved before you start putting offers on homes.

Filling out the pre-qualification form is a simple process. After providing your contact information, you’ll be asked to give RBC permission to access your credit score. Doing this won’t affect your credit score.

You’ll be prompted to enter a potential home value as well as the amount of money you have saved up for a down payment. If you haven’t made an offer on a home yet, you won’t know what to enter for “Purchase Price”. That’s okay. You don’t have to fill out that field to continue.

It’s a good idea to enter your total down payment savings into the “Proposed Down Payment” space, though. It’s not necessary, but it’s useful information for your RBC mortgage specialist to have.

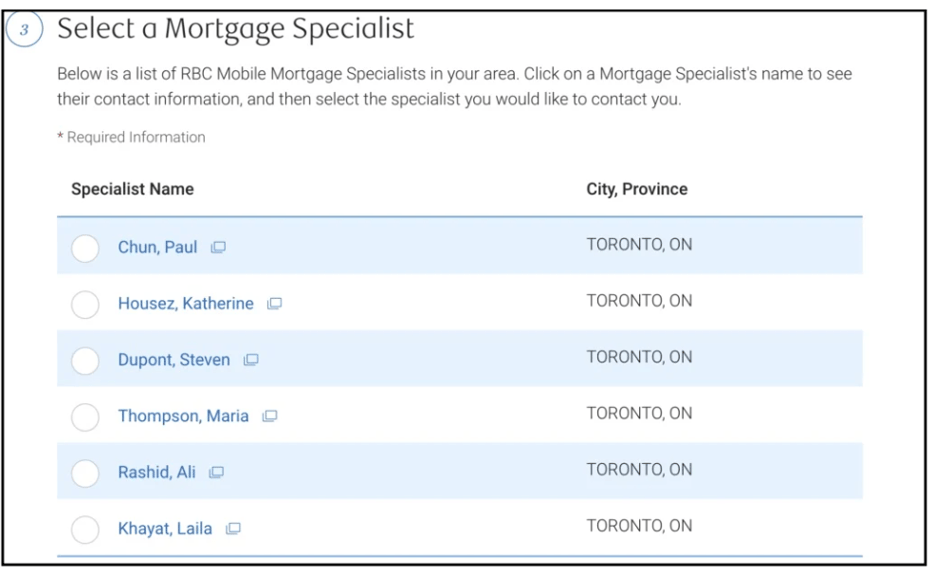

You’ll then choose a nearby mortgage specialist to help you with the rest of your pre-approval.

Who you choose to work with shouldn’t be a make-or-break decision — they’ll all be offering the same products and using the same qualification guidelines.

Frequently asked questions

What is RBC’s prime rate today?

What is RBC’s prime rate today?

RBC’s prime rate is currently 4.45%. This rate determines the interest the bank charges on variable-rate mortgages, lines of credit and certain credit cards.

Can you negotiate mortgage rates at RBC?

Can you negotiate mortgage rates at RBC?

You can — and should — negotiate your mortgage rate at RBC. When you first apply for a mortgage, a lender may not offer you the lowest rate possible, so it’s always advisable to ask for a lower one. Even if you’re only able to reduce the cost of your mortgage by a little, the money you save can be put toward a better use.

DIVE EVEN DEEPER

Kurt Woock

Kurt Woock

Clay Jarvis

Clay Jarvis

Georgia Rose

Georgia Rose Clay Jarvis

Clay Jarvis